HDB Financial Services IPO Analysis: Before, During & After Listing

HDB Financial Services IPO: A Complete Analysis — Before, During, and After the Listing

India's financial services landscape witnessed a landmark moment in mid-2025 when HDB Financial Services Limited — one of the country's most anticipated unlisted giants — finally crossed the threshold from private to public. For investors in the unlisted/pre-IPO market, this was a story years in the making. This blog breaks down the complete IPO journey of HDB Financial Services: what it looked like before the IPO, how it unfolded during the subscription window, and what the listing data tells us about the road ahead.

Part 1: HDB Financial Services — Before the IPO

Company Background

HDB Financial Services Limited (HDBFS) was incorporated on June 4, 2007 under the Companies Act, 1956, and commenced lending operations on July 31, 2007. It is a wholly-owned subsidiary of HDFC Bank — India's largest private sector bank — which held a 94.36% promoter stake prior to the IPO.

Classified by the Reserve Bank of India (RBI) as an Upper Layer NBFC (NBFC-UL), the company earned top-tier credit ratings of CARE AAA and CRISIL AAA for its long-term debt obligations — a strong signal of balance sheet credibility. It ranked as the 7th largest NBFC in India by total gross loan book.

Business Model: Three Lending Verticals

HDB Financial Services operates through a diversified, retail-focused lending model structured around three core verticals:

Enterprise Lending (39.30% of loan book): Loans to micro, small, and medium enterprises (MSMEs) — the engine room of India's credit-hungry informal economy. This was the first vertical launched in 2008.

Asset Finance (38.03% of loan book): Secured loans for commercial vehicles, construction equipment, and tractors, catering to the backbone of India's infrastructure and logistics sectors.

Consumer Finance (22.66% of loan book): A blend of secured and unsecured personal loans, consumer durable loans, and related products targeting India's rising aspirational class.

Beyond lending, the company also provides BPO services (back-office support, collection services) to its parent HDFC Bank and distributes insurance products to its lending customers, creating additional fee income streams.

Distribution Network: "Phygital" at Scale

One of HDBFS's most cited moats is its omni-channel distribution model, combining physical branches with digital capabilities. As of March 31, 2025, the company operated 1,771 branches across 1,162 towns in 31 states and union territories, with over 80% of branches located outside major metropolitan areas. It also maintained partnerships with over 80 brands and OEMs, and an external dealer network of over 140,000 retailer and dealer touchpoints.

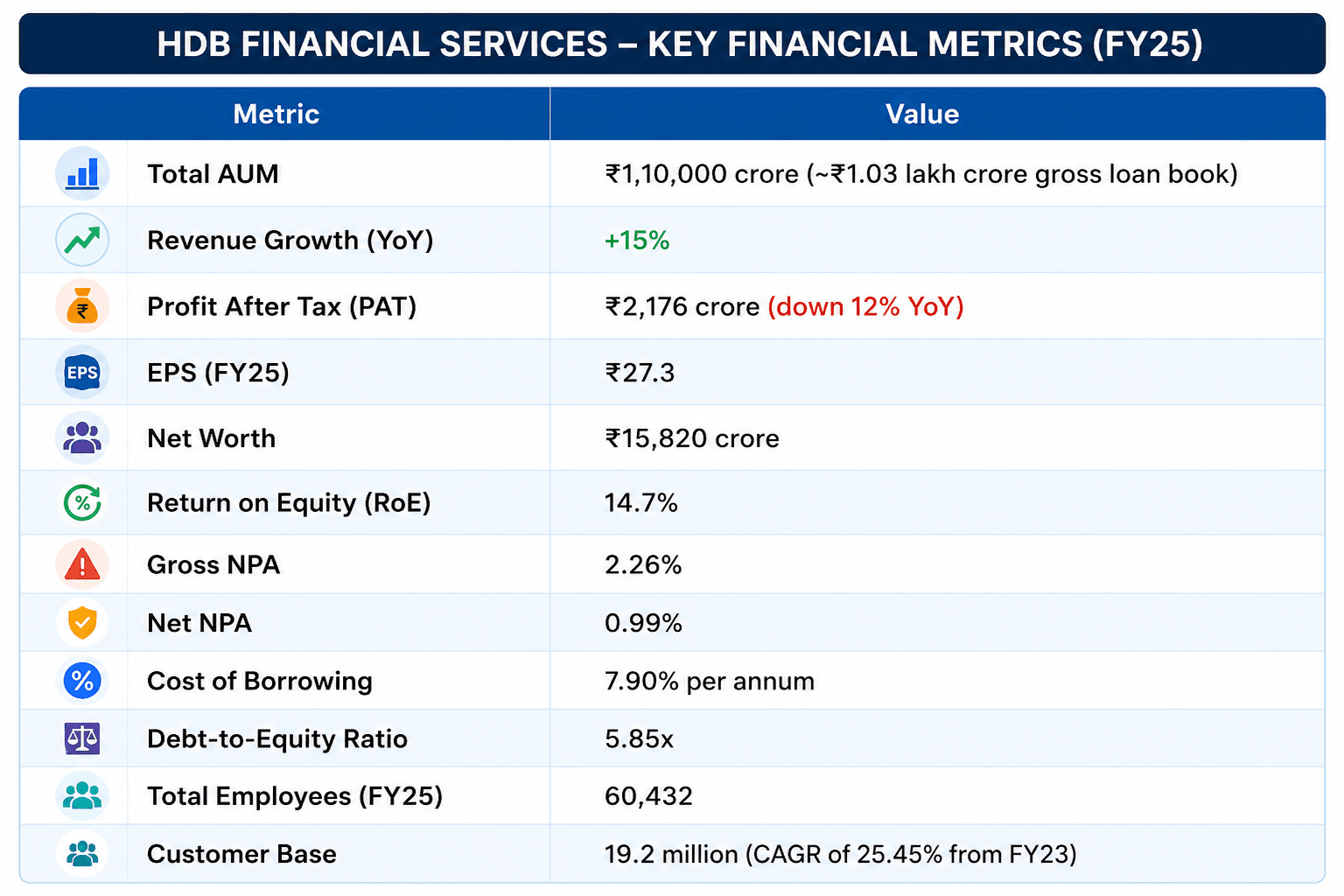

Key Financial Metrics (FY25)

The PAT decline of 12% in FY25 was primarily driven by a near-doubling of impairment provisions to ₹2,113 crore — a precautionary step amid rising interest rate volatility and stress in certain unsecured loan segments. Revenue, however, remained resilient with a 15% topline growth, and the gross loan book grew at a CAGR of 23.54% between FY23 and FY25, reflecting strong business momentum.

The Unlisted Market Phase

Prior to the DRHP filing, HDB Financial Services shares were actively traded in India's unlisted/pre-IPO market. Early investors — typically employees, anchor investors, and savvy wealth management clients — held shares at prices significantly above the eventual IPO band. As IPO buzz intensified post-DRHP filing, unlisted prices climbed toward the ₹1,200+ range, though analysts at the time cautioned that such prices implied valuations well above comparable listed NBFCs.

This divergence between unlisted market pricing and the eventual IPO price band was a key talking point for advisors guiding clients in the pre-IPO space.

DRHP Filing and SEBI Approval

HDB Financial Services filed its Draft Red Herring Prospectus (DRHP) with SEBI on October 30, 2024, signalling the company's formal intent to go public. After thorough regulatory review, SEBI granted its approval on May 28, 2025, clearing the path for one of India's most-awaited IPOs of the year.

Part 2: During the IPO — Subscription, Pricing, and Investor Response

IPO Structure and Key Details

Parameter | Detail |

Issue Size | ₹12,500 crore |

Fresh Issue | ₹2,500 crore (3.38 crore shares) |

Offer for Sale (OFS) | ₹10,000 crore (13.51 crore shares, by HDFC Bank) |

Price Band | ₹700 – ₹740 per share |

Face Value | ₹10 per share |

Lot Size | 20 shares |

Minimum Retail Investment | ₹14,800 (at upper band) |

IPO Open Date | June 25, 2025 |

IPO Close Date | June 27, 2025 |

Allotment Date | June 30, 2025 |

Listing Date | July 2, 2025 |

Stock Exchange | BSE & NSE |

Registrar | MUFG Intime India Pvt. Ltd. (Link Intime) |

The 10 Book Running Lead Managers (BRLMs) included JM Financial, BNP Paribas, BofA Securities India, Goldman Sachs (India), HSBC Securities, IIFL Capital Services, Jefferies India, Morgan Stanley India, Motilal Oswal, Nomura, Nuvama Wealth, and UBS Securities — a marquee line-up befitting the scale of this issue.

Anchor Allocation

Before the public subscription opened, HDB Financial Services raised ₹3,369 crore from anchor investors on June 24, 2025 — a strong institutional vote of confidence ahead of the IPO.

Subscription Data

The IPO saw polarised participation across investor categories:

Category | Subscription |

Qualified Institutional Buyers (QIBs) | 55.47x |

Non-Institutional Investors (NIIs/HNIs) | 9.99x |

Retail Individual Investors (RIIs) | 1.41x |

Employees | 5.72x |

The near-zero oversubscription in the retail segment reflected the common hesitation around large-cap IPOs where listing pops are perceived to be modest. However, QIB interest at 55x confirmed that institutional investors viewed the HDFC Bank-backed NBFC as a high-quality, long-duration holding.

A special Shareholder Quota was also available: any investor holding at least one share of HDFC Bank on or before June 19, 2025 was eligible to apply under this category (up to ₹2,00,000 worth of shares).

Grey Market Premium (GMP)

Heading into listing, the grey market premium (GMP) for HDB Financial Services hovered between ₹72–₹75 per share, suggesting a listing pop of approximately 10% over the issue price — broadly consistent with what eventually materialised.

Use of Proceeds

The fresh issue proceeds of ₹2,500 crore were earmarked for:

Deploying funds into lending and investment activities across retail and enterprise segments

Repaying existing borrowings to optimise capital structure

Supporting technology upgrades, infrastructure investment, and general corporate purposes

The OFS component (₹10,000 crore) was entirely HDFC Bank's partial stake monetisation and did not flow to HDB Financial Services.

Part 3: After the IPO — Listing Performance and Long-Term Outlook

Listing Day: A Strong Debut

On July 2, 2025, HDB Financial Services made its stock market debut on both BSE and NSE. The stock listed at ₹835 per share — a 12.84% premium over the IPO price of ₹740. By end of day, shares settled at approximately ₹840–₹841, delivering a listing gain of close to 14% for allottees.

Bloomberg reported that this was the second-best listing-day performance by any Indian IPO since 2010 that raised at least $1.5 billion — a remarkable achievement that put to rest concerns about large-cap IPOs underperforming on debut.

For retail investors who applied at the minimum lot size of 20 shares, the listing gain translated to approximately ₹1,900 per lot on the day of listing.

Post-Listing Investor Strategy: What Analysts Recommend

Market experts were broadly aligned on the post-listing strategy for HDB Financial Services shareholders:

For allottees: Most brokerage firms recommended holding for the long term. The stock was characterized as a "portfolio stock" — a company to hold across market cycles given the strength of its promoter backing, diversified loan book, and India's expanding credit market narrative.

For non-allottees: Analysts suggested waiting for price stabilization over the first 3–6 months before entering. Given the large issue size and modest retail oversubscription, price discovery was expected to be gradual rather than explosive.

Key Risks to Monitor Post-Listing

Any honest post-IPO analysis of HDB Financial Services must acknowledge the headwinds alongside the tailwinds:

Rising NPAs: The net NPA rose from 0.63% in FY24 to 0.99% in FY25, while the gross NPA climbed to 2.26%. While still within an acceptable range for NBFC peers, the trajectory bears watching — especially given the near-doubling of provisions in FY25.

PAT Compression: Despite healthy revenue growth, the 12% decline in FY25 PAT was a setback. FY26 performance will be crucial in demonstrating whether the company can control credit costs while sustaining loan book expansion.

Regulatory Risk: A draft RBI circular from October 2024 on "Forms of Business" has the potential to affect HDBFS's relationship with its parent HDFC Bank, particularly where lending products overlap. While not an immediate threat, this remains a structural overhang worth tracking.

Competitive Landscape: HDB Financial Services holds roughly 2.22% market share by AUM in an intensely competitive NBFC landscape. Rivals like Bajaj Finance (0.44% net NPA, 19.2% RoE) and Cholamandalam (0.97% net NPA, 19.8% RoE) outperform on key return metrics, keeping valuation headroom tight.

Valuation Consideration: At the IPO price of ₹740, the implied price-to-book (P/B) was approximately 3x on FY26E book value — a fair but not cheap entry point. The "HDFC badge premium" was widely acknowledged to be priced in.

The Long-Term Bull Case

Despite near-term challenges, the long-term investment thesis for HDB Financial Services remains compelling for several reasons:

India's credit penetration story is still in its early chapters. The NBFC sector's growth is being propelled by rising urbanisation, formalisation of the economy, and increasing financial inclusion in Tier 2–4 cities — exactly the market where HDBFS has the deepest roots.

With 80%+ of branches outside metros, an 18–19 million strong customer base (CAGR of ~28% since 2020), and an AAA-rated funding franchise backed by India's largest private bank, HDB Financial Services is structurally positioned to compound steadily over the next decade.

The BPO and insurance distribution segments — while small today — offer additional revenue diversification as the company matures in the public markets.

Summary: The HDB Financial Services IPO at a Glance

Phase | Key Highlight |

Pre-IPO | DRHP filed Oct 2024; traded in unlisted market at ₹1,200+; 7th largest NBFC; FY25 AUM ~₹1.10 lakh crore |

During IPO | ₹12,500 crore issue; price band ₹700–₹740; QIBs subscribed 55.47x; anchors raised ₹3,369 crore |

Post-IPO | Listed at ₹835 (12.84% premium); closed ~₹840; 2nd-best large IPO debut since 2010; "hold for long-term" consensus |

Final Thoughts

The IPO of HDB Financial Services was a defining moment for India's NBFC sector — proof that quality businesses with strong parentage, deep distribution networks, and a well-managed retail loan book can attract serious institutional capital even in a high-interest-rate environment.

For investors who had exposure to HDB Financial Services through unlisted shares at reasonable entry prices, the listing delivered meaningful returns. For those entering post-listing, patience and a multi-year investment horizon appear to be the market consensus.

At We Grow Wealth, we closely track pre-IPO and unlisted opportunities like HDB Financial Services to help our clients participate in India's wealth-creation journey — before they become mainstream.

Disclaimer: This blog is for informational and educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Please consult a SEBI-registered investment advisor before making any investment decisions. Data referenced is sourced from publicly available DRHP/RHP filings, SEBI, NSE, BSE, and reputed financial research platforms.

HDB Financial Services IPO: A Complete Analysis — Before, During, and After the Listing

India's financial services landscape witnessed a landmark moment in mid-2025 when HDB Financial Services Limited — one of the country's most anticipated unlisted giants — finally crossed the threshold from private to public. For investors in the unlisted/pre-IPO market, this was a story years in the making. This blog breaks down the complete IPO journey of HDB Financial Services: what it looked like before the IPO, how it unfolded during the subscription window, and what the listing data tells us about the road ahead.

Part 1: HDB Financial Services — Before the IPO

Company Background

HDB Financial Services Limited (HDBFS) was incorporated on June 4, 2007 under the Companies Act, 1956, and commenced lending operations on July 31, 2007. It is a wholly-owned subsidiary of HDFC Bank — India's largest private sector bank — which held a 94.36% promoter stake prior to the IPO.

Classified by the Reserve Bank of India (RBI) as an Upper Layer NBFC (NBFC-UL), the company earned top-tier credit ratings of CARE AAA and CRISIL AAA for its long-term debt obligations — a strong signal of balance sheet credibility. It ranked as the 7th largest NBFC in India by total gross loan book.

Business Model: Three Lending Verticals

HDB Financial Services operates through a diversified, retail-focused lending model structured around three core verticals:

Enterprise Lending (39.30% of loan book): Loans to micro, small, and medium enterprises (MSMEs) — the engine room of India's credit-hungry informal economy. This was the first vertical launched in 2008.

Asset Finance (38.03% of loan book): Secured loans for commercial vehicles, construction equipment, and tractors, catering to the backbone of India's infrastructure and logistics sectors.

Consumer Finance (22.66% of loan book): A blend of secured and unsecured personal loans, consumer durable loans, and related products targeting India's rising aspirational class.

Beyond lending, the company also provides BPO services (back-office support, collection services) to its parent HDFC Bank and distributes insurance products to its lending customers, creating additional fee income streams.

Distribution Network: "Phygital" at Scale

One of HDBFS's most cited moats is its omni-channel distribution model, combining physical branches with digital capabilities. As of March 31, 2025, the company operated 1,771 branches across 1,162 towns in 31 states and union territories, with over 80% of branches located outside major metropolitan areas. It also maintained partnerships with over 80 brands and OEMs, and an external dealer network of over 140,000 retailer and dealer touchpoints.

Key Financial Metrics (FY25)

The PAT decline of 12% in FY25 was primarily driven by a near-doubling of impairment provisions to ₹2,113 crore — a precautionary step amid rising interest rate volatility and stress in certain unsecured loan segments. Revenue, however, remained resilient with a 15% topline growth, and the gross loan book grew at a CAGR of 23.54% between FY23 and FY25, reflecting strong business momentum.

The Unlisted Market Phase

Prior to the DRHP filing, HDB Financial Services shares were actively traded in India's unlisted/pre-IPO market. Early investors — typically employees, anchor investors, and savvy wealth management clients — held shares at prices significantly above the eventual IPO band. As IPO buzz intensified post-DRHP filing, unlisted prices climbed toward the ₹1,200+ range, though analysts at the time cautioned that such prices implied valuations well above comparable listed NBFCs.

This divergence between unlisted market pricing and the eventual IPO price band was a key talking point for advisors guiding clients in the pre-IPO space.

DRHP Filing and SEBI Approval

HDB Financial Services filed its Draft Red Herring Prospectus (DRHP) with SEBI on October 30, 2024, signalling the company's formal intent to go public. After thorough regulatory review, SEBI granted its approval on May 28, 2025, clearing the path for one of India's most-awaited IPOs of the year.

Part 2: During the IPO — Subscription, Pricing, and Investor Response

IPO Structure and Key Details

Parameter | Detail |

Issue Size | ₹12,500 crore |

Fresh Issue | ₹2,500 crore (3.38 crore shares) |

Offer for Sale (OFS) | ₹10,000 crore (13.51 crore shares, by HDFC Bank) |

Price Band | ₹700 – ₹740 per share |

Face Value | ₹10 per share |

Lot Size | 20 shares |

Minimum Retail Investment | ₹14,800 (at upper band) |

IPO Open Date | June 25, 2025 |

IPO Close Date | June 27, 2025 |

Allotment Date | June 30, 2025 |

Listing Date | July 2, 2025 |

Stock Exchange | BSE & NSE |

Registrar | MUFG Intime India Pvt. Ltd. (Link Intime) |

The 10 Book Running Lead Managers (BRLMs) included JM Financial, BNP Paribas, BofA Securities India, Goldman Sachs (India), HSBC Securities, IIFL Capital Services, Jefferies India, Morgan Stanley India, Motilal Oswal, Nomura, Nuvama Wealth, and UBS Securities — a marquee line-up befitting the scale of this issue.

Anchor Allocation

Before the public subscription opened, HDB Financial Services raised ₹3,369 crore from anchor investors on June 24, 2025 — a strong institutional vote of confidence ahead of the IPO.

Subscription Data

The IPO saw polarised participation across investor categories:

Category | Subscription |

Qualified Institutional Buyers (QIBs) | 55.47x |

Non-Institutional Investors (NIIs/HNIs) | 9.99x |

Retail Individual Investors (RIIs) | 1.41x |

Employees | 5.72x |

The near-zero oversubscription in the retail segment reflected the common hesitation around large-cap IPOs where listing pops are perceived to be modest. However, QIB interest at 55x confirmed that institutional investors viewed the HDFC Bank-backed NBFC as a high-quality, long-duration holding.

A special Shareholder Quota was also available: any investor holding at least one share of HDFC Bank on or before June 19, 2025 was eligible to apply under this category (up to ₹2,00,000 worth of shares).

Grey Market Premium (GMP)

Heading into listing, the grey market premium (GMP) for HDB Financial Services hovered between ₹72–₹75 per share, suggesting a listing pop of approximately 10% over the issue price — broadly consistent with what eventually materialised.

Use of Proceeds

The fresh issue proceeds of ₹2,500 crore were earmarked for:

Deploying funds into lending and investment activities across retail and enterprise segments

Repaying existing borrowings to optimise capital structure

Supporting technology upgrades, infrastructure investment, and general corporate purposes

The OFS component (₹10,000 crore) was entirely HDFC Bank's partial stake monetisation and did not flow to HDB Financial Services.

Part 3: After the IPO — Listing Performance and Long-Term Outlook

Listing Day: A Strong Debut

On July 2, 2025, HDB Financial Services made its stock market debut on both BSE and NSE. The stock listed at ₹835 per share — a 12.84% premium over the IPO price of ₹740. By end of day, shares settled at approximately ₹840–₹841, delivering a listing gain of close to 14% for allottees.

Bloomberg reported that this was the second-best listing-day performance by any Indian IPO since 2010 that raised at least $1.5 billion — a remarkable achievement that put to rest concerns about large-cap IPOs underperforming on debut.

For retail investors who applied at the minimum lot size of 20 shares, the listing gain translated to approximately ₹1,900 per lot on the day of listing.

Post-Listing Investor Strategy: What Analysts Recommend

Market experts were broadly aligned on the post-listing strategy for HDB Financial Services shareholders:

For allottees: Most brokerage firms recommended holding for the long term. The stock was characterized as a "portfolio stock" — a company to hold across market cycles given the strength of its promoter backing, diversified loan book, and India's expanding credit market narrative.

For non-allottees: Analysts suggested waiting for price stabilization over the first 3–6 months before entering. Given the large issue size and modest retail oversubscription, price discovery was expected to be gradual rather than explosive.

Key Risks to Monitor Post-Listing

Any honest post-IPO analysis of HDB Financial Services must acknowledge the headwinds alongside the tailwinds:

Rising NPAs: The net NPA rose from 0.63% in FY24 to 0.99% in FY25, while the gross NPA climbed to 2.26%. While still within an acceptable range for NBFC peers, the trajectory bears watching — especially given the near-doubling of provisions in FY25.

PAT Compression: Despite healthy revenue growth, the 12% decline in FY25 PAT was a setback. FY26 performance will be crucial in demonstrating whether the company can control credit costs while sustaining loan book expansion.

Regulatory Risk: A draft RBI circular from October 2024 on "Forms of Business" has the potential to affect HDBFS's relationship with its parent HDFC Bank, particularly where lending products overlap. While not an immediate threat, this remains a structural overhang worth tracking.

Competitive Landscape: HDB Financial Services holds roughly 2.22% market share by AUM in an intensely competitive NBFC landscape. Rivals like Bajaj Finance (0.44% net NPA, 19.2% RoE) and Cholamandalam (0.97% net NPA, 19.8% RoE) outperform on key return metrics, keeping valuation headroom tight.

Valuation Consideration: At the IPO price of ₹740, the implied price-to-book (P/B) was approximately 3x on FY26E book value — a fair but not cheap entry point. The "HDFC badge premium" was widely acknowledged to be priced in.

The Long-Term Bull Case

Despite near-term challenges, the long-term investment thesis for HDB Financial Services remains compelling for several reasons:

India's credit penetration story is still in its early chapters. The NBFC sector's growth is being propelled by rising urbanisation, formalisation of the economy, and increasing financial inclusion in Tier 2–4 cities — exactly the market where HDBFS has the deepest roots.

With 80%+ of branches outside metros, an 18–19 million strong customer base (CAGR of ~28% since 2020), and an AAA-rated funding franchise backed by India's largest private bank, HDB Financial Services is structurally positioned to compound steadily over the next decade.

The BPO and insurance distribution segments — while small today — offer additional revenue diversification as the company matures in the public markets.

Summary: The HDB Financial Services IPO at a Glance

Phase | Key Highlight |

Pre-IPO | DRHP filed Oct 2024; traded in unlisted market at ₹1,200+; 7th largest NBFC; FY25 AUM ~₹1.10 lakh crore |

During IPO | ₹12,500 crore issue; price band ₹700–₹740; QIBs subscribed 55.47x; anchors raised ₹3,369 crore |

Post-IPO | Listed at ₹835 (12.84% premium); closed ~₹840; 2nd-best large IPO debut since 2010; "hold for long-term" consensus |

Final Thoughts

The IPO of HDB Financial Services was a defining moment for India's NBFC sector — proof that quality businesses with strong parentage, deep distribution networks, and a well-managed retail loan book can attract serious institutional capital even in a high-interest-rate environment.

For investors who had exposure to HDB Financial Services through unlisted shares at reasonable entry prices, the listing delivered meaningful returns. For those entering post-listing, patience and a multi-year investment horizon appear to be the market consensus.

At We Grow Wealth, we closely track pre-IPO and unlisted opportunities like HDB Financial Services to help our clients participate in India's wealth-creation journey — before they become mainstream.

Disclaimer: This blog is for informational and educational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Please consult a SEBI-registered investment advisor before making any investment decisions. Data referenced is sourced from publicly available DRHP/RHP filings, SEBI, NSE, BSE, and reputed financial research platforms.