When Blue Chips Stop Compounding: 23 BSE 100 Giants Delivered 5% or Less in 3 Years

Keywords: BSE Sensex, large cap returns, blue chip stocks India, HDFC Bank, RIL, TCS, HUL

A headline in the Economic Times recently stopped many long-term investors in their tracks: 23 companies from the BSE 100 — including RIL, TCS, HUL, and HDFC Bank — delivered 5% or less in total returns over three years. For names that collectively anchor every large-cap mutual fund, every Nifty 50 SIP, and virtually every "safe" equity portfolio in India, this is a number that deserves serious attention.

This isn't a market crash story. The BSE Sensex itself hasn't collapsed. But beneath the headline index, something important has been quietly playing out — a tale of valuation gravity, earnings disappointment, and structural transitions that have trapped some of India's most trusted names in a multi-year consolidation phase.

The BSE Sensex Paradox: Index Up, Individual Stocks Flat

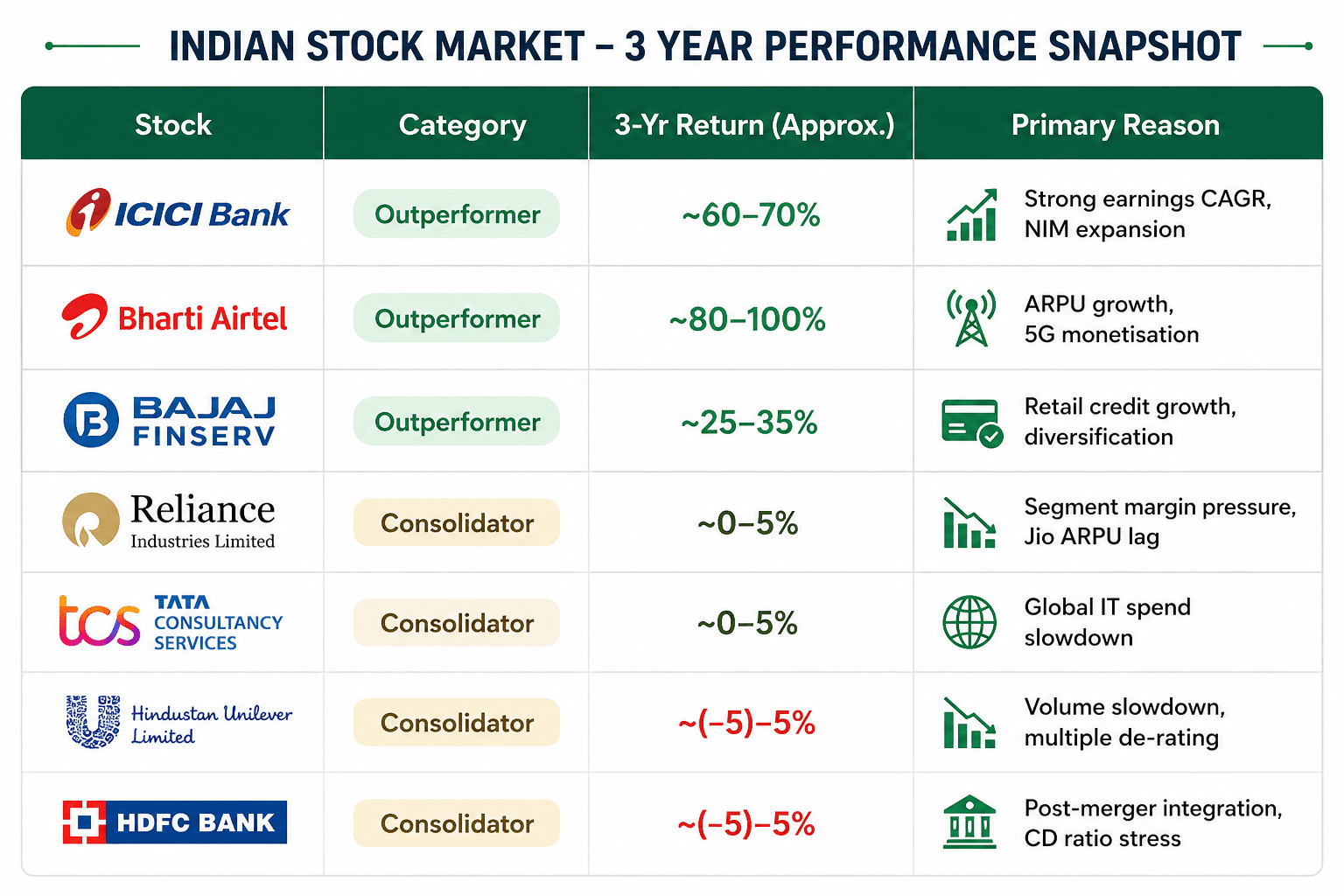

The BSE Sensex is often cited as the barometer of Indian equity markets. But an index is a weighted average — and when that average is pulled up by a concentrated set of outperformers (Airtel, ICICI Bank, Bajaj Finance, select PSU stocks), it can easily mask the stagnation of the rest.

That's exactly what has happened. While the BSE Sensex notched incremental gains over the 2022–2025 period, nearly a quarter of the BSE 100's constituent companies delivered sub-bank-FD returns to their shareholders. In an environment where even liquid funds were yielding 6–7%, these large-cap stalwarts simply didn't pay.

Why India's Most Recognisable Stocks Went Nowhere

Reliance Industries (RIL)

RIL is India's largest company by market capitalisation and a cornerstone of the BSE Sensex. Yet the stock has been in a prolonged consolidation since mid-2021, with the refining-to-retail-to-telecom conglomerate struggling to generate fresh re-rating catalysts. The O2C (Oil to Chemicals) business faced margin pressure as global refining spreads narrowed. Jio's ARPU growth, while positive, came slower than the market had priced in. Retail, despite massive store additions, saw profitability pressures from rapid expansion. Jio's IPO filing in June 2026 may finally unlock the value the stock has been sitting on.

TCS

India's largest IT company and a perennial favourite for long-term wealth creation ran headlong into a structural slowdown in global technology spending. As Western economies tightened monetary policy aggressively through 2022–2024, discretionary IT budgets at client companies were the first to be cut. TCS, Infosys, and Wipro all saw revenue growth decelerate sharply — and for a stock trading at 28–32x earnings, even a temporary growth slowdown creates significant valuation compression. TCS's 3-year return tells a story of a fundamentally sound business that was, quite simply, priced for perfection at the peak.

HUL (Hindustan Unilever)

HUL's underperformance is perhaps the most telling of all. The FMCG bellwether — a "defensive" stock in every portfolio manager's playbook — ran into a perfect storm: rural demand weakness, premiumisation headwinds from inflationary pressure on consumers, and intense competition from D2C brands and regional players. For years, HUL traded at 60–70x earnings — a "quality premium" that investors were willing to pay for earnings predictability. When volume growth slowed and that predictability was questioned, the multiple contracted sharply. The business remained strong. The valuation simply had nowhere to go.

HDFC Bank

HDFC Bank's story is the most complex of the four. The merger with HDFC Ltd in July 2023 — India's largest-ever financial sector merger — created a balance sheet behemoth but also introduced significant integration complexity. The merged entity faced elevated credit-to-deposit (CD) ratios, slower-than-expected deposit growth, and margin pressure as it digested the HDFC Ltd loan book. FII ownership in HDFC Bank hit a multi-decade low through much of 2024–2025. The stock, which had been a 5-year compounder for a generation of investors, essentially went sideways for three years.

What This Tells Us About BSE Sensex Investing

1. Brand is not a moat against valuation compression. RIL, TCS, HUL, and HDFC Bank are not failing businesses. Their revenues grew, their balance sheets remained clean, and their market positions stayed intact. What they suffered was the gravitational pull of high starting valuations. The BSE Sensex, in its present composition, includes many stocks that entered this zone of valuation risk post-2020.

2. The index can lie about portfolio health. A retail investor watching the BSE Sensex hit 80,000 in 2024 and 85,000 in 2025 might reasonably assume their large-cap portfolio was doing the same. The index's weightage mechanism means a handful of outperformers can drag the headline number upward even as 23 components languish.

3. Earnings growth, not story, drives long-term price. Each of the four stocks had a compelling long-term narrative. But over a 3-year window, what actually moved prices was earnings growth — or the absence of it. Companies that maintained 15–20%+ earnings CAGRs (ICICI Bank, Bajaj Finance, Airtel) created wealth. Companies that didn't,didn't.

The Outperformers vs. The Consolidators (2022–2025)

Should You Worry? A Balanced View

The honest answer is: not necessarily — but you should be aware. Three-year underperformance in fundamentally strong businesses has historically been followed by periods of strong outperformance, as earnings catch up to expectations and valuations reset to more reasonable levels.

HDFC Bank at 2.5x book is a very different risk/reward than HDFC Bank at 3.5x book. HUL at 50x earnings with rural recovery underway is meaningfully more attractive than HUL at 70x earnings with volumes stagnating. Several of these 23 names may now be in exactly the kind of mean-reversion setup that long-term investors should find interesting.

What Investors Should Do

Review starting valuations before labelling something "safe." A PSU bank at 1x book and an FMCG stock at 65x earnings carry very different risk profiles — regardless of which one sounds safer at a dinner table.

Diversify across the return spectrum. In the same 3-year window where these 23 BSE Sensex names stagnated, mid-cap and small-cap indices delivered 15–20% CAGRs. A portfolio anchored entirely in "safe" large caps would have substantially underperformed.

Don't confuse holding period with patience. Holding a fundamentally deteriorating business for 3 years is not patience — it's inertia. Holding a fundamentally sound business through a valuation reset is patience. Know which one you're doing.

Watch for the earnings inflection. For HDFC Bank, that may come as CD ratios normalise and NIMs recover. For RIL, Jio's IPO listing may be the catalyst. For TCS, a global IT spending revival as AI-led transformation projects scale. The earnings inflection — not the BSE Sensex level — will be the signal.

The Bottom Line

Twenty-three companies from the BSE 100 delivering sub-5% returns over three years is not a story of market failure. It is a story of what happens when good companies enter multi-year windows of valuation excess, and the market quietly corrects that excess through time rather than through a crash.

The BSE Sensex will continue to compound. The companies within it will continue to grow. But as this headline makes clear, owning the right companies at the right price remains the core discipline of equity investing — no matter how familiar the names, and no matter how blue the chips.